我们不再支持这个浏览器. 使用受支持的浏览器将提供更好的体验.

请 更新浏览器.

从行业领袖到政策制定者, people across the country and across the aisle are discussing the gender pay and wealth gap, 以及政府和雇主的解决方案,如育儿假政策. 利用我们独特的, 高频镜头, the 澳博官方网站app 研究所 examined some of the gender gaps in financial outcomes across a range of indicators, 包括金融弹性方面的差异, 医疗保健支出, 参与在线平台经济作为收入平滑工具, 以及女性拥有的小企业的表现.

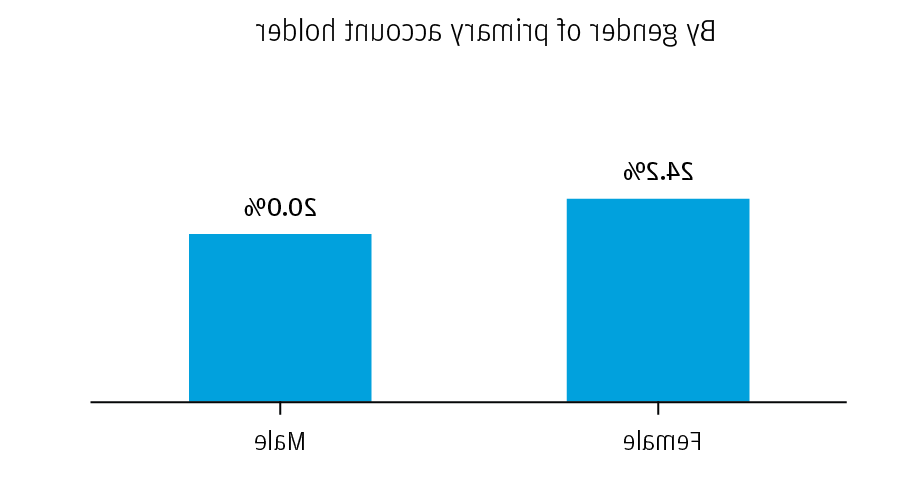

一般, 女性 face discrepancies compared to their male counterparts across a range of financial outcomes. 在我们的报道中 财务结果中的性别差距:医疗支付的影响, we leveraged consumer account data to compare the financial outcomes of accounts held by 女性 versus men. 第一个, 特别是, 而大多数主要账户持有人是男性(54%), 低收入的主要账户持有人更有可能是女性. 重要的是, 女性账户持有人的实得收入水平大约低20%, 支出, 流动资产比男性帐户持有人多(图1). 尽管他们的循环信用卡债务水平略低, 与收入相比,女性的信用卡债务负担也略高于男性.

图1: 女性账户持有人收入较低, 支出, and liquid assets and higher revolving credit card debt burden than male account holders

Our research on out-of-pocket 医疗保健支出 further illustrates financial gender gaps. 横跨美国的23个州 医疗保健自付支出小组在美国,女性承担的医疗支出负担略高,为2%.他们的税后收入的0%用于医疗保健,而这一比例为1%.男性占6%. 重要的是, 我们表明,自付医疗费用对家庭来说可能是严重的,并且与他们财务生活的其他方面有着错综复杂的联系. 这对女性来说尤其如此.

我们发现,当家庭受到经济困难的打击时,性别差距仍然存在, 比如额外的医疗费用. We define extraordinary 医疗支付s as 支出 on 医疗保健服务 in a given month that were at least $400, 超过年收入的1%, and more than 2 standard deviations away from the individuals’ normal monthly mean healthcare expenses. 我们对 超额医疗费用的后果 shows that the mean value of extraordinary payments was 18 percent lower in dollar terms for 女性 than for men ($1,女性为714美元,而女性为2美元,男士99英镑). 然而, 作为月收入的一小部分, 妇女的特别医疗费数额更大, 女性占每月实得工资的52%,而男性占48%, even though the incidence of extraordinary 医疗支付s across genders in any given year is roughly the same (图2).

图2以美元计算,妇女的特别医疗费用的平均数额要低得多,但在其每月实得收入中所占比例较高.

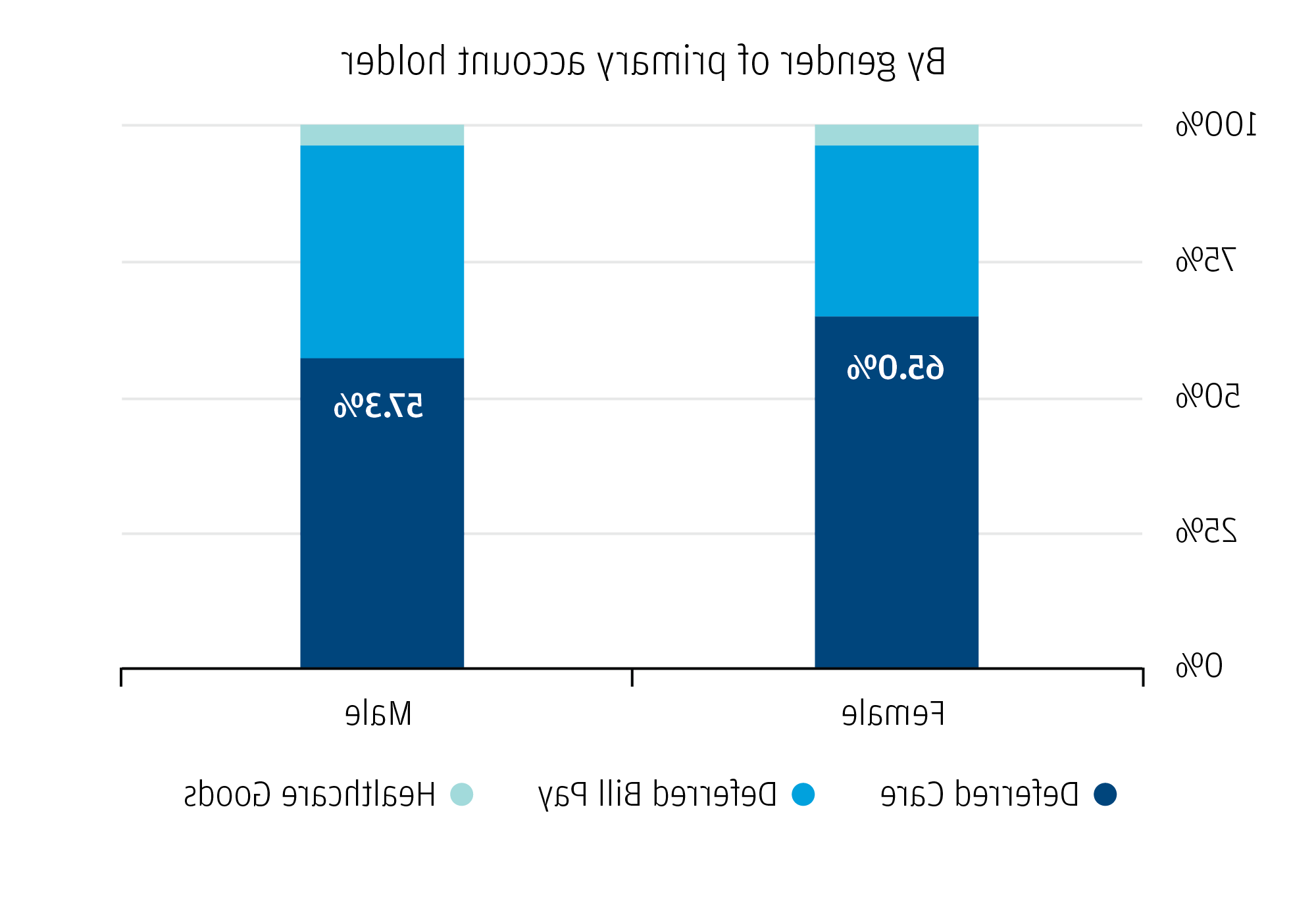

特别医疗支付对女性账户持有人的财务结果的影响大于男性账户持有人(图3). 在付款前立即付款, 与男性相比,女性在流动资产方面的增幅要大得多, suggesting they were more likely to delay the payment or to defer seeking treatment until they were able to pay for it. 与男性相比,女性的收入和资产水平较低, these findings suggest that 女性 were in a weaker financial position than men to withstand an extraordinary payment. 事实上, 付款一年后, 女性的循环信用卡债务仍比以前高出14%, 相比之下,男性仅增长了3%, indicating that the gender gap in financial outcomes had only widened after the payment hit.

图3: 在支付医疗费用之前,妇女的流动资产显著增加,在支付特殊医疗费用一年后,妇女的循环信用卡债务水平更高.

另外, 我们发现医疗保健支出对现金流事件很敏感, 对女性来说尤其如此. We 观察到的 a 60 percent increase in out-of-pocket 医疗保健支出 in the week after families received a tax refund, 在75天的时间里,医疗费用保持了大约20%的增长. 重要的是, 流动资产非常有限的家庭——低于600美元——在退税到来后,医疗支出的增幅是那些超过3美元的家庭的20倍,流动资产500美元.

此外, 我们将展示 在退税到来后的75天内,女性增加支出的比例(24%)高于男性(20%)(图4)。. 对于女性来说,在退税到来后,医疗保健支出增加的更大份额代表了递延医疗保健——在女性账户持有人中,65%的退税触发的医疗保健支出是在医疗保健提供者那里进行的,而在男性账户持有人中,这一比例为57%(图5)。.

图4: 抵税后退税, female account holders increased their healthcare expenditures to a greater degree than male account holders

退款后75天内医疗保健支出增加百分比

图5: 与男性账户持有人相比,女性账户持有人的递延医疗支出在退税引发的医疗支出中所占比例更大

按类型划分的支出响应百分比

综上所述, these findings highlight the critical role liquid assets play in determining not only when people pay for, 还要消费, 医疗保健服务. They suggest that the link between physical and financial health may be particularly strong for 女性. 它们还强调了制定和实施提高妇女抵御金融波动能力的政策和解决办法的重要性, 包括医疗费用. 例如, 两个重要的政策问题是:第一, whether periodic tax payments would reduce the deferral of 医疗保健服务 throughout the year, 和第二, whether there might be a way to increase the flexibility with which families pay for 医疗保健服务. To the extent that healthcare and other 支出 needs may arise outside of tax refund season, 将一年中最大的现金流事件之一限定在这个时间范围内,实际上保证了一些人将不得不推迟医疗,直到他们的退税到来.

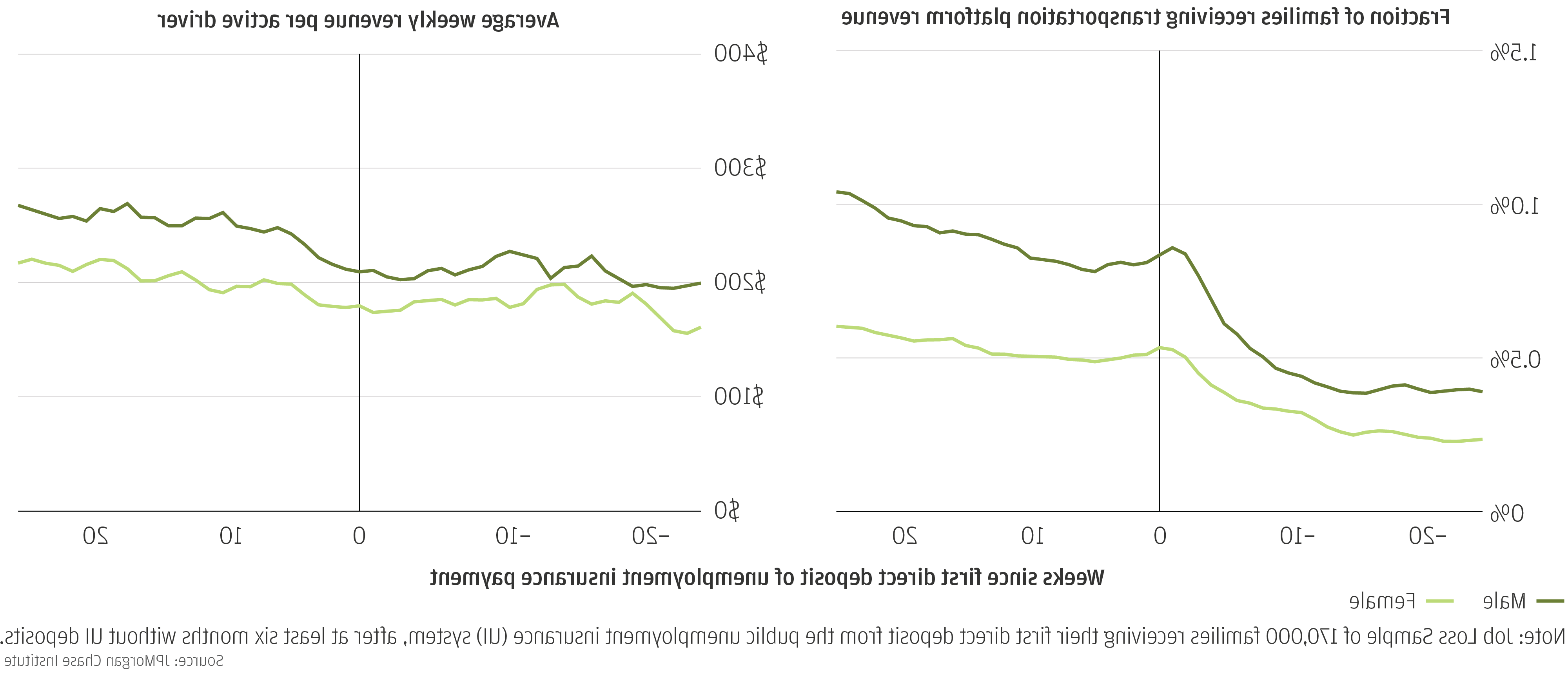

进一步研究家庭如何应对经济困难, 我们探讨了家庭如何使用在线平台经济作为收入平滑工具. 在我们的报道中 Bridging the Gap: How Families Use the Online Platform Economy to Manage their Cash Flow, 我们利用澳博官方网站app研究所在线平台经济数据集来探讨性别差异,并将分析限制在交通运输部门, 在非自愿失业后,大多数家庭最有可能转向哪里. 我们的目的是了解我们是否存在性别差异 以前观察到的 在交通平台参与方面——平台司机主要是男性——坚持家庭使用交通平台,以通过失业来平衡收入.

我们跟踪了非自愿失业事件前后的平台参与情况, 以一个家庭第一次领取失业保险的收据来表示. 在下面的图6中, 左图证实,在主要账户持有人为男性的家庭中,使用交通平台的人数增加得更快. 右图显示,两类家庭的人均收入保持稳定,尽管在领取第一笔失业保险金的前几周,参保率有所上升, 结果在整个期间男女收入差距稳定在30美元左右.. 值得注意的是,这一差距在几周后会扩大到50美元左右.

换句话说, the Online Platform Economy may be more available as an income-smoothing tool between jobs for men than for 女性. 在某种程度上,这种差异可能反映了结构性差异, 这或许值得政策制定者和平台提供商关注.

图6: 与女性账户持有人相比,男性账户持有人在失业时,交通平台参与度和平均每周收入的增长幅度更大

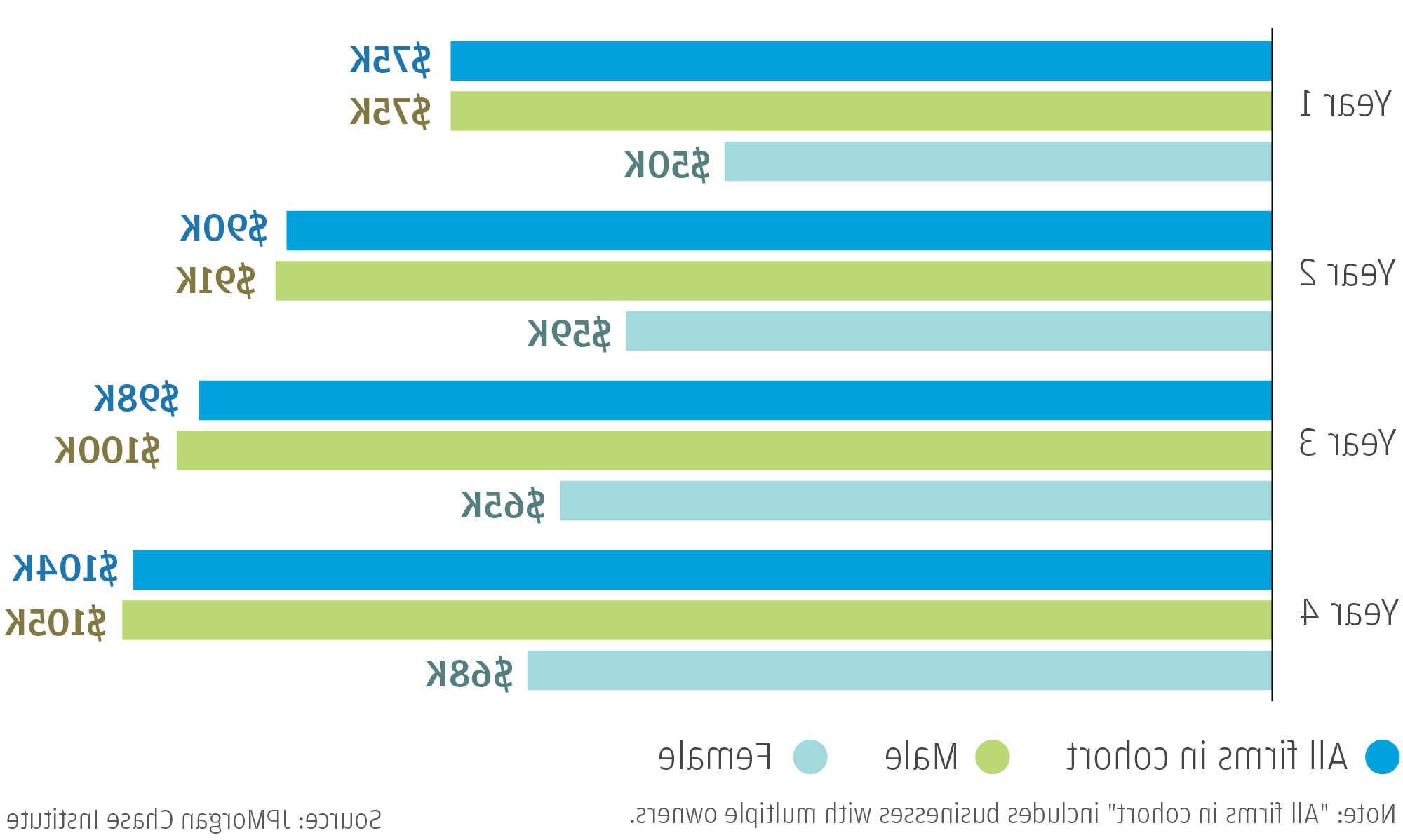

The 研究所’s research has also explored gender disparities in the small business sector. 在我们的报告中, 性别、年龄和小企业财务结果, 我们发现,小型企业的增长轨迹和财务结果在很大程度上取决于所有者的人口结构. 女性-owned small businesses have 34 percent lower first-year revenues than male-owned businesses, 生成50美元,第一年就有1000英镑, 而男性拥有的公司只有75美元,第一年的收入是1000万. 这种差异随着公司的成长而持续存在, 女性拥有的公司创造了68美元,他们在第四年的收入达到了1000万美元, 与104美元相比,男性拥有的公司则是1000万.

图7: 2013年小企业收入中位数,按性别和年份分列

另外, 女性-owned small businesses are underrepresented among firms that leverage external financing to drive growth, representing only 18 percent of small businesses that rely substantially on external financing. 然而, 尽管收入下降,增长放缓, 女性拥有的企业与男性拥有的企业的存活率相同.

Targeted solutions that support 女性-owned small business success would not only contribute to reducing gender inequalities, but policies that help 女性 start larger businesses and grow their businesses could have a material impact on the U.S. 经济. 女性拥有的企业和男性拥有的企业一样有可能存活下来, 但由于收入增长较低,它们开始规模较小,并一直保持较小的规模, 对经济的影响相对较小. 如果女性拥有的企业开始时的收入水平与男性拥有的企业相同,并且经历了相同的收入增长水平, they would substantially increase the overall economic contributions of the small business sector to the U.S. 经济.

结论与启示

These insights contribute to a larger narrative of marginalized groups experiencing disproportionate financial burdens, 我们的研究强调,政策制定者和决策者需要在未来的努力中考虑女性的经历. 医疗保健 and tax policies can offer more flexibility in when families receive their tax refund and pay for healthcare; platform providers and regulators should consider the gender disparity in transportation platform participation and consider ways to support 女性 utilizing this important income-smoothing tool; and policies, 非营利组织, and businesses ought to support and finance 女性-owned small businesses as an investment in economic growth. 这些发现让人们对美国的性别不平等有了新的认识, and the JPMC 研究所 will continue to investigate these dynamics across financial themes.

澳博官方网站app & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. 请 review its website terms, privacy and security policies to see how they apply to you. 澳博官方网站app & Co. 不负责(也不提供)任何产品, 该第三方网站或应用程序的服务或内容, 明确带有澳博官方网站app字样的产品和服务除外 & Co.